Debt Funding: Instruments to Raise Capital Effectively

As of 31 March 2023, the national debt of India stood at ₹155.6 lakh crore, accounting for a whopping 57.1% of our GDP. 😳 This means that every citizen in India has an average debt of more than ₹1 lakh.

Debt has been the bearer of bad news and hardship for individuals and businesses alike. But the financial experts argue that it can actually be leveraged to our advantage.

The difference lies in associating the term “leverage” with “debt”. The Collins English Dictionary defines leverage as “to use borrowed money in order to buy it or pay for investments or assets.” (No, borrowing from a mafia to play poker doesn't count! 😉)

That's what we will be discussing in this article. A kind of leverage where a company (or an individual) borrows money to invest or contribute to other debts and then pays off later with interest. This is known as debt funding or debt financing. It is the magic trick which allows the swap of the negative concept of "being in debt" to utilising it as "leverage for better use". 😎

Yes, you read that right. Debt, when managed strategically, can be transformed into a powerful tool for financial success. All you need to do is capitalise on it and then simply feast on the fruit of positive returns in investments. 🍎

Curious about how we can do this? Let’s begin with learning the many…

Instruments (Types) of Debt Funding

/content-assets/0817cc42a0fd483b955065059ab3d5d2.jpeg)

Fixed Income Assets

Fixed-income assets fall under the long-term options for debt funding. The kind of cash inflows given by the lender that includes a fixed interest along with the principal amount comes in the “fixed income” asset class.

The following are the primary debt instruments under this particular class.

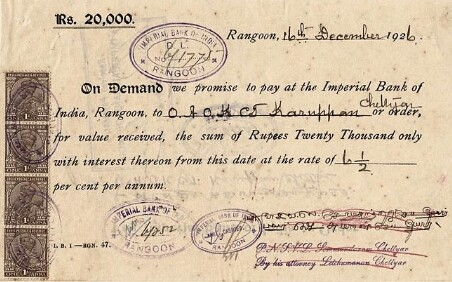

a. Bonds:

A Bond is a debt security where the issuer provides a loan to the holder and is mandated to pay cash inflows as per the terms. When you buy a bond, you are essentially lending money to the issuer, who promises to repay you the principal amount (aka the face value or par value) plus interest over a set period.

It is very similar to the kind of written commitments or an I.O.U (abbreviation for I Owe You) people make while taking or giving loans to others. Imagine a piece of paper with terms & conditions jotted down along with the details for the borrowed amount and the return date. 📑

That’s what a bond is, only in a far more formal format provided by official organisations like the government or large companies.

Now, the question arises…

How do Companies Utilise Bonds to Raise Money?

What a large corporation does is, whenever it needs capital for a new project or investing in assets, it issues bonds of varying interest rates to the public. Since a fixed income (interest + principal amount) is promised, the public buys these bonds, and companies receive a sort of loan as desired.

Learn in-depth about how bonds are a good sign for your investment portfolio by clicking here.

b. Debentures

Debentures are long-term debts that don't have the backing of collateral. Initially, debentures were symbolised as a kind of acknowledgement of a debt, but today, it is represented as one of the debt instruments.

A debenture is thus akin to a certificate of loan or a loan bond that attests to the company's obligation to repay a specified amount with interest. The interest rate here is definitely fixed, along with the principal amount. Superficially, debentures look similar to bonds, which raises the question…

Why do some companies issue debentures instead of bonds?

Companies with solid finances issue debentures to avoid diluting equity shares. Since the funds raised through debentures become part of the company's capital structure, they don't become share capital.

Since debentures don't have any collateral backing, only large corporations with strong reputations can successfully issue them. People applying for these debentures do so based on the company's creditworthiness, which could be a bit riskier.

Learn what other factors isolate debentures from bonds and further crucial details about them by clicking here.

c. Loan:

The whole concept of debt is often interconnected with loans, but both slightly differ from each other. Loan involves borrowing or lending money, whereas debt can consist of money, properties, bonds, services, etc. Hence, a loan is a kind of debt that is strictly associated with capital.

Individuals, businesses, and even governments take loans to initiate new projects, pay off other debts, or get a service. Home loans, student loans, car loans, etc., are some of the most common forms of loans.

Here, a borrower takes a fixed sum from a lender based on a fixed interest rate (or no interest when borrowed informally). The amount is utilised for varying purposes and gets added to the entity’s list of bill payments till the loan’s tenure.

Utilise this instrument to the best of your ability by knowing it from myriad aspects. Click here and select the right loan option for you.

d. Mortgage:

Whether in old movies or growing up, you must have heard the term “girvi rakhna”, right? That’s what a mortgage loan, one of the most common instruments in this list, is about. This secured loan is not limited to big organisations or government agencies. Ordinary citizens like you and I have been using this instrument for centuries.

Mortgage refers to borrowing a large sum of money by keeping a fixed asset like real estate as collateral.

Read What is a Mortgage Loan? to get acquainted with all the details you might have missed about this particular instrument.

After fixed-income assets, it’s time to check out another type of debt instrument. Rookie investors mostly prefer this next kind of debt instrument as they tend to have a much smaller tenure and are more easily available. 👍

Money Market Instruments

Money market instruments are medium to short-term debt instruments that enhance a business’ financial liquidity. These instruments have a much less maturity period, high liquidity, and low risk.

a. Treasury Bills:

A debt instrument issued by the government, the Treasury Bill or T-Bill, was introduced by the Reserve Bank of India. These bills have the sole purpose of fulfilling the government's short-term capital demand. They are issued in three tenors: 91 days, 182 days, and 364 days.

Here are India’s recent Treasury Bills over 31 days. 👇

/content-assets/57ea097d9c0c41ef8a0f4dc82afd20ab.png)

Treasury Bills are considered one of the safest money market instruments as the government is the backer. For in-depth information, read the article What are Treasury Bills in India?

b. Commercial Paper:

This short-term debt instrument is issued by corporations for payrolls, inventories, and accounts payables. Commercial papers are typically unsecured loans lacking any support from collaterals. Though they offer a higher yield than treasury bills, they are a much riskier debt instrument.

Commercial paper allows raising funds in large amounts, and its regulation falls under RBI’s jurisdiction. Hence, companies with good to excellent credit scores are allowed to issue them.

c. Repurchase Agreements

Also known as Repo, a Repurchase Agreement is a financial transaction that is self-explanatory from the name. Here, one party sells securities to another with the agreement to repurchase them at a later date at a predetermined price.

How do Repos Work?

-

The seller agrees to sell the securities to the buyer (usually investors) by forming an agreement and receiving capital from the buyer in exchange for the securities. The seller then transfers the securities to the buyer.

-

The seller agrees to repurchase the securities at a later date. The repurchase price is typically lower than the market price of the securities. This difference in price is called the repo rate.

-

The buyer holds the securities as collateral. The collateral ensures that the buyer will be repaid if the seller defaults on the agreement.

The Bottom Line

That's it for debt funding and its instruments. Remember, instead of viewing debt as a burden, try to embrace it as an opportunity. By doing so, we would be one more step closer to transforming the humongous national debt mentioned earlier from a symbol of financial strain into a catalyst for economic growth. After all, finding light in darkness is what hope means, right? 💡

How was this article?

Like, comment or share.

3